1. What is GSTR 1?

GSTR 1 is a monthly return that should be filed by every registered dealer. It contains details of all outward supplies i.e sales.

GSTR-1 has a total of 13 sections.

2. Why is GSTR 1 important?

GSTR 1 contains details of all the sales transactions of a registered dealer for a month.

The GSTR 1 filed by a registered dealer is used by the government to auto populate GSTR 3 for the dealer and GSTR 2A for dealers to whom supplies have been made.

GSTR-1 should be filed even if there is nil returns to be filed (no business activity) in the given taxable period.

3. When is GSTR 1 due?

Latest Update:

As per GST Council meeting of 9th September 2017

| Return | Month | Revised due date | Additional comments |

| GSTR-1 | July 2017 | 10-Oct-17 | 3rd October for persons with turnover more than Rs. 100 crores |

Due dates for filing of returns for August, September onwards will be notified later by the government.

As per Notification No. 29/2017 dated 5th September 2017

| Month | Due Date for Filing GSTR-1 |

| July 2017 | Upto 10th September |

| August 2017 | Upto 5th October |

| September 2017 onwards | 10th of next month |

4. Who should file GSTR 1?

Every registered person is required to file GSTR 1 irrespective of whether there are any transactions during the month or not.

The following registered persons are exempt from filing GSTR 1:

- Input Service Distributors

- Composition Dealers

- Suppliers of online information and database access or retrieval services (OIDAR), who have to pay tax themselves (as per Section 14 of the IGST Act)

- Non-resident taxable person

- Tax payer liable to collect TCS

- Tax payer liable to deduct TDS

6. How to revise GSTR 1?

GSTR 1 once filed cannot be revised. Any mistake made in the return can be revised in the next months return. It means that if a mistake is made in September GSTR 1, rectification for the same can be made in October’s GSTR 1.

7. Details to be provided in GSTR 1

2. Legal name of the registered person: Name of the taxpayer will be auto-populated at the time of logging into the common GST Portal.

3. Aggregate Turnover in the preceding Financial Year and for April to June 2017: Aggregate Turnover is total value of all taxable supplies made (excluding the value of inward supplies on which tax is payable by a person on reverse charge basis), exempt supplies, exports of goods or services or both.

4. Taxable outward supplies made to registered persons (including UIN-holders): All B2B supplies should be mentioned in this section.

4A. Under this head invoice wise details of all supplies made other than those under reverse charge and supplies made through e-commerce operator should be mentioned in this section.

4B. All outward supplies on which reverse charge is applicable and which has been excluded in 4A should be shown here

4C. Supplies made through e-commerce operator which attract TCS has to be reported here. The details have to be rate wise or operation wise

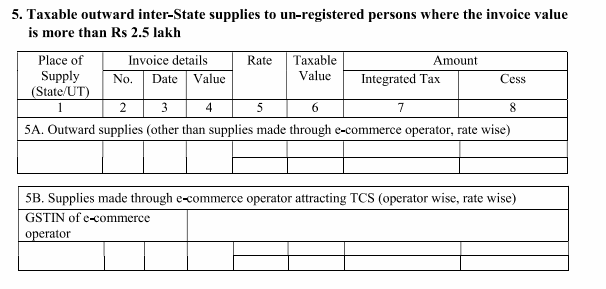

5. Taxable outward inter-State supplies to un-registered persons where the invoice value is more than Rs 2.5 lakh

Invoice wise details of all supplies made to unregistered dealers is to be mentioned here:

5A. This will include B2B invoices i.e. sale to unregistered dealer and

5B. The details of B2C supplies made online through e-commerce operator

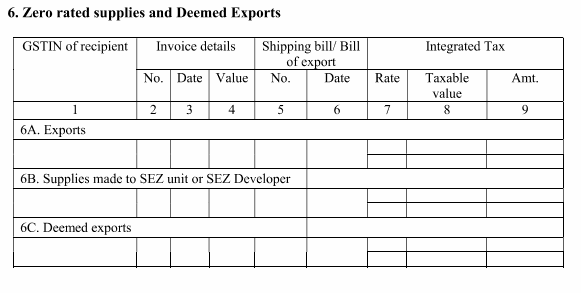

6. Zero-rated supplies and deemed exports:

All type of zero-rated supplies, exports, deemed exports (supply to SEZ, EOUs) has to be mentioned under this head. A registered dealer has to give details of invoice, bill of export or shipping bill.

7. This section contains a rate wise summary of all sales made during the month.

7A. All sales including sales made through e-commerce operator has to be mentioned here. Also separate mention of supplies made through e-commerce operator should be declared here

7B. B2C interstate supply along with place of supply i.e. name of state where invoice value is upto Rs 2.5 lakhs should be specified here

8. Nil-rated, exempt and non-GST outward supplies:

All the other supplies whether nil rated, exempt or non-GST which has not been reported under any of the above needs to be reported under this head. This need to be further bifurcated into Inter-State, Intra-State to registered and unregistered persons.

9. Amendments to taxable outward supply details furnished in returns for earlier tax periods in table 4, 5 and 6 (including current and amended debit notes, credit notes, and refund vouchers):

Any correction to sales data submitted in the return of previous months pertaining to registered dealers can be done by filling in this section.

All debit notes, credit notes and refund voucher should also be entered here

10. Amendments to taxable outward supplies to unregistered persons furnished on returns for earlier tax periods:

Point 9 was for details of supplies to registered dealer furnished in previous returns. This point is for making correction to regarding details of unregistered dealers both B to B and B to C provided in earlier returns.

11. Consolidated Statement of Advances Received or adjusted in the current tax period, plus amendments from earlier tax periods.

- Mention all advances received during the earlier period corresponding to invoices raised during the current period.

- In this table, specify all advances received in the month for which invoice was not raised

12. HSN-wise summary of outward supplies: This section requires a registered dealer to provide HSN wise summary of goods sold.

13. Documents issued during the tax period: This head will include details of all invoices issues in a tax period, any kind of revised invoice, debit notes, credit notes etc.

Comments

Post a Comment